A review of alternative Lending Models for Passive Income generation. Speculate at your own risk but do not prey on students.

Everyone Wants To Be A Venture Capitalist

And, since 2005 with technology platforms bringing small businesses and venture capital investment opportunities to a broader audience, you can be one too.

This is an interesting and relatively new option for creating a passive income stream.

There are two main types of alternative lending. Peer-to-Peer (P2P) lending and Balance Sheet Lending.

Alternative Lending: Peer-to-Peer

P2P lending brings formality to financial arrangements between borrowers and investors through electronic arrangements make through an intermediary.

This is a business relationship with 3-parties. The borrower, the intermediary, and the lender.

In this relationship, you, the lender accepts both the risk and the return on investment. Placing your capital at risk and benefiting from interest payments.

The initial and pure peer-to-peer lending concepts involved cutting out traditional financial institutions like banks. And, connecting potential borrowers directly with individual investors.

In this model, the intermediary, offers origination, loan servicing and recovery services. In addition, the intermediary charges fees for these services.

Pure P2P lending platforms have a transparent cost structure.

As P2P lending platforms grew, and as investment dollars grew in this sector; the P2P lending platforms and traditional banks started getting involved.

In early ventures it was a business relationship with 3-parties. Consequently, once banks began getting involved it created a business relationship with 4-parties. Borrower, P2P Lending Platform, Lender and the ‘partner bank’.

Alternative Lending: Balance Sheet

The 4-party business relationship created balance sheet lending. Sometimes called portfolio lending. This model shifts the risk in the venture and increases the cost structure of obtaining capital.

In this model, the P2P Lending platform is required to have a banking license. And, these transactions are closer to traditional bank lending.

In these balance sheet lending transactions, the P2P lending platform purchases the loan note from the bank and carries the loan on its balance sheet.

Consequently, the P2P lending platform has assumed the risk of the loan and the costs associated with loan default.

You, the investor, are dealing with the P2P lending platform. The borrower repays the P2P lending platform who in turn pays you the investor for use of your capital. Confusing?

Balance sheet lending does not have a transparent cost structure. In addition, there are increased costs associated with securing the capital and insuring against default.

How Do You Know?

How do you know if you are investing in a pure P2P loan or a balance sheet transaction? Find out where the capital for the loan came from. Was the loan funded from the P2P market or from the balance sheet of the P2P platform?

And, If the lending platform is offering you buyback guarantees or other insurance products that guarantee repayment of your capital you are looking at a balance sheet loan.

There is a broad base of lender choice in peer-to-peer investment platforms. You can choose to invest in a pool of loans. Orm you can select individuals, specific sectors, or specific projects to invest your capital in.

If you invest your capital into a pool of loans through the peer lending platform you simply indicate the level of default risk which you will accept. Accordingly, this determines your return on investment.

The higher the risk accepted by the lender the higher the return.

The risk classification of the loan is based on the venture and credit rating of the business/borrower.

Investment Policy Basics

This is where I must bring you back to basic investment policy. Our primary interest is to protect against loss of capital. Secondary to this, is ensuring an adequate return on investment that contributes to your passive income.

P2P Lending and balance sheet lending as passive income generators are speculative ventures.

Guidelines If You Choose Alternative Lending

In order to protect your capital from loss, you must diversify your peer-lending portfolio, ensure your investment choices are within strong business sectors, with business owners who have strong credit ratings, and if possible the venture is backed by some form of insurance or government program.

You must review each individual investment opportunity on their own merits.

If your peer-to-peer lending is a mortgage for the borrower, the borrower must have a strong credit rating and the underlying asset (house) must be in a strong real estate market. If strong real estate markets still exist.

High Risk

If you choose to invest 10% of your portfolio in high risk investments and those investments are P2P loans, ensure that you have a base of at least 20 loans within that 10% of your capital.

I would choose 20 individual loans/mortgages/projects and research the business/people you are investing in.

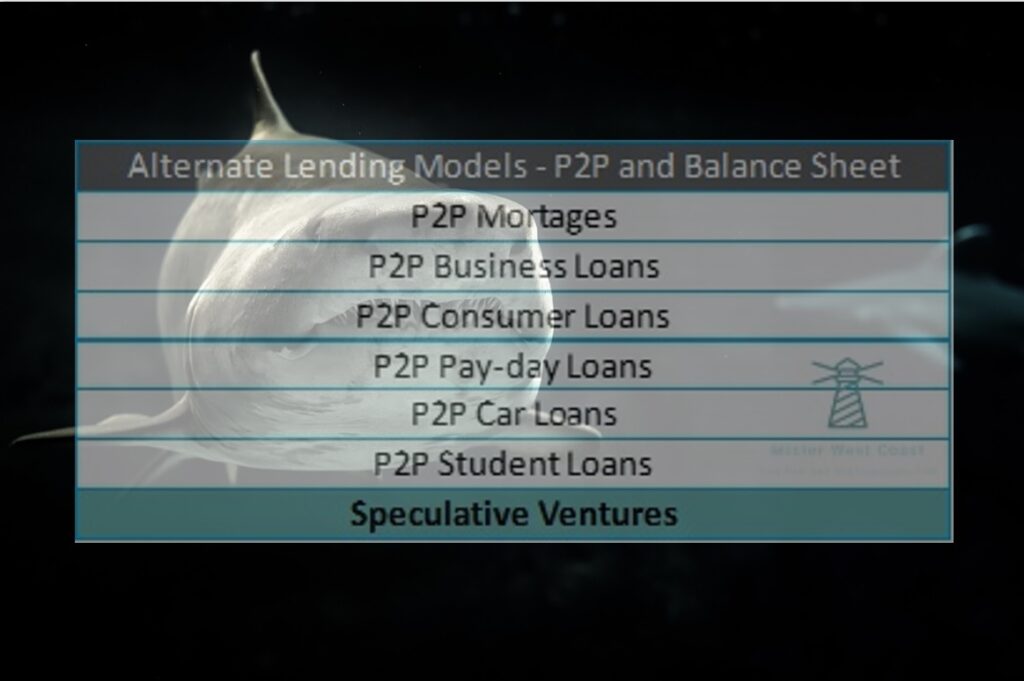

In conclusion, there are now many peer-lending platforms available where someone with capital can invest in a variety of ventures including:

- Mortgages – may include whole mortgage or pooled mortgages

- Business Ventures including Business Loan, Equipment Lease, Cash Advance against Credit Card Income, Commercial Mortgage, Equipment Purchase Loan, Business Credit Consolidation Loan

- Consumer/pay-day loans

- Car loans

- Student Loans*

*If you are in a fortunate position where you live from passive income and you choose to prey on students to generate more passive income, you found the wrong guy to follow. I will write again on student loans and an idea related to Financial Mastery Rule 11: You Give.

Borrowing is not much better than begging; just as lending with interest is not much better than stealing.

Doris Lessing

Additionally, all of our posts in the Personal Finance Series can be found here.

Finally, more great content can be discovered on our Youtube channel.

<<Previous Next>>